|

|

#181

03-01-2021, 04:22 PM

03-01-2021, 04:22 PM

|

|||

|

|||

|

Re: How much money needed to Retire?

CAVEAT EMPTOR

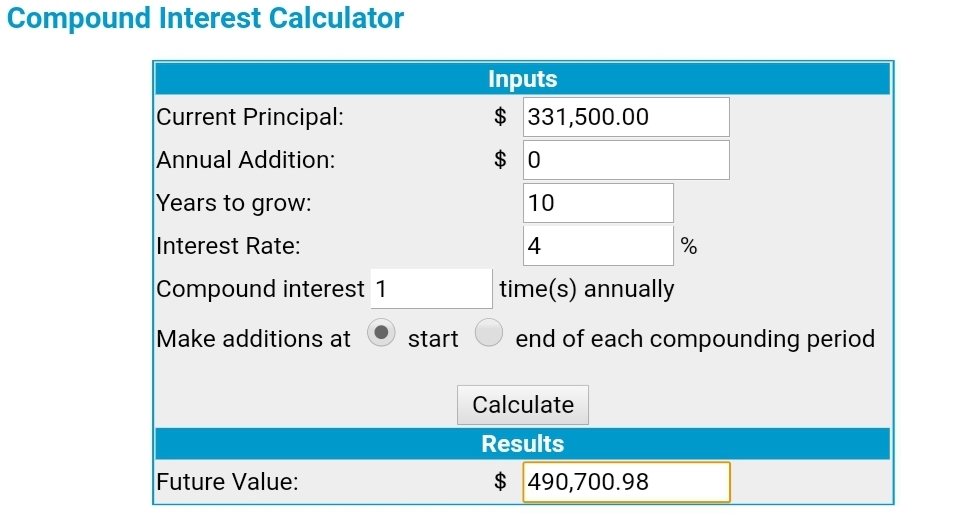

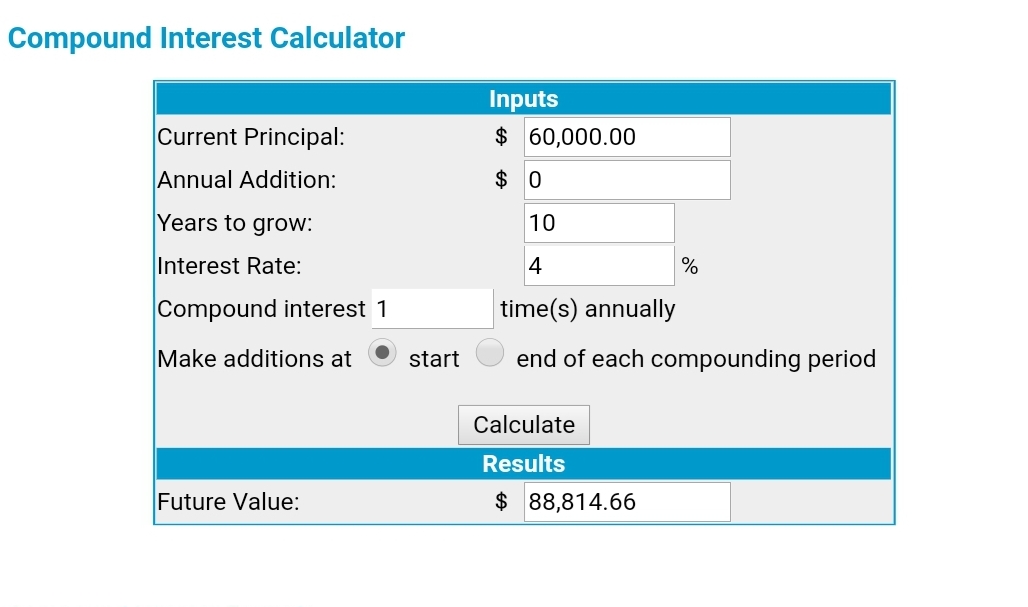

Tan Ooi Boon Invest Editor How you can make up to $1 million with CPF To start the new year on a positive note, here are some tips on how you can invest your money so that you can reap returns of between $200,000 and $1 million for your retirement. The best part is you do not even need to come up with a lot of cash to earn this amount, and you can start planning for this investment right now in your own home. No, this is not one of those "too good to be true" get-rich-quick schemes that you may come across on social media. Indeed, this investment is not only for all residents here, it is also the safest around because it is protected by the Singapore Government. I am referring to the ubiquitous Central Provident Fund (CPF). Many people are still unsure how to maximise its full potential to generate good retirement income that will last them a lifetime. Singaporeans have had a love-hate relationship with the CPF. Those in the hate camp are resolute in seeing CPF as a "scam" by the Government to prevent them from withdrawing all their funds at age 55. As they detest receiving their payouts in "dribs and drabs" from 65, many have the mistaken belief that they should deplete their accounts as much as possible, such as by using all their eligible funds to pay for their housing loan. After all, since they cannot touch much of the money until 65, they think it is better to use CPF to pay their mortgages, as this means they can have more cash now. But fans of CPF think otherwise - they are mostly savers and even savvy financial planners who know how to use CPF's ability to generate good returns for themselves. It is not an exaggeration to say that CPF has been making millionaires out of ordinary working-class Singaporeans who will get to enjoy every dollar that they put there, with hardly any risk of losing even a cent. Of course, such big returns will not appear overnight - you need a lifetime of patience and some planning to reap the rewards. Lifelong income for retirement There is a reason that Singapore's CPF is lauded as the best retirement scheme in Asia. CPF Life, its longevity annuity scheme, can provide a rather substantial monthly payout for life with a relatively low investment. For instance, those who turn 55 this year can set aside the Enhanced Retirement Sum (ERS) of $279,000 from either their CPF Special Account (SA) or Ordinary Account (OA) to enjoy a monthly payout of up to $2,300 from the age of 65. If they live until 85, they would have received about $550,000 in all, which means they would have almost doubled their original amount and gained more than $270,000. At 90, they would have received a total of about $690,000, or more than $410,000. Do not despair if you do not have enough for ERS - you can still aim for the Full Retirement Sum at $186,000, which will give you a monthly payout of up to $1,500, or the Basic Retirement Sum (BRS) at $93,000, which will give you a monthly payout of up to $800. Of course, when you set aside a lower amount for CPF Life, you will receive lower returns than those who have put up the highest sum. If you are still keen to earn more, the good news is that this investment does not end at 55. You can continue to top up the CPF Life retirement account with either cash or your remaining funds in CPF until you hit the ERS limit for the year. How to gain more In the past few years, many savvy CPF fans have been proudly sharing their secret of how to "game" the CPF system by making use of its own rules to make more money. This is how one tip works: A few months before you reach 55, you will receive a written notice from the CPF Board to inform you of the CPF Life scheme and how you can benefit from it. Once you decide that you want to set aside the ERS, the total sum of $279,000 will be deducted from your existing funds in the SA first. If you do not have enough, the remaining sum will come from your OA. You should know by now that money in the SA earns 4 per cent interest, while money in the OA earns 2.5 per cent. Of course, those seeking more returns would prefer that CPF deduct the ERS amount from the OA first, rather than the SA, but this is not how the current process works. To circumvent the deduction from the SA, you can leave behind the mandatory minimum of $40,000 and invest the rest in a short-term and relatively safe investment product approved under the CPF Investment Scheme. When the time for deduction comes, only the remaining $40,000 in your SA will be deducted and the CPF Board has to deduct the rest of the sum for ERS from your OA. After the deduction, you can cash out on your short-term investment and all the money will then go back to your SA, which earns more interest. You may want to commend the person who first thought of this creative plan to "hide money" from the deduction process so that members get to have more funds in their SA. But this plan comes with some risks, especially if you are not a savvy investor. First, you need to pick the right investment product and pay the applicable fees even though you plan to park the SA funds for only a short time. Know that no matter how safe a product is, there will still be risks of losses, especially if a major crisis breaks out suddenly. So it may not be worth your while just to earn extra interest at 4 per cent. Do not forget that if you leave your money untouched in the OA, it still earns 2.5 per cent. Smarter way to gain profit There is another CPF rule that you can make use of, so that you can leave more money in both the SA and OA. This is how you do it: When it is your time to set aside your retirement sum, choose the lowest possible tier - the BRS, which is $93,000 this year. When the transfer date comes, only this amount will be deducted from your SA, leaving the rest of your funds in the SA intact. No money will be deducted from the OA. After this happens, you can "change your mind" and top up your retirement account to hit ERS, but with cash. Why top up your retirement account with cash and not CPF? It is not easy to find risk-free investments that can give a yield of 2.5 per cent, let alone 4 per cent. If you have accumulated substantial balances in your OA and SA, this method allows you to enjoy the maximum returns in CPF by keeping most of your initial sums intact. If you continue to leave all your money in CPF after 55 and withdraw only sparingly, substantial balances can yield a return of $500,000, if not more, by the time you hit 85, given the high interest rate. And together with your returns from the CPF Life payouts, you can aim to hit $1 million. After all, we should prosper as we live longer, and not get poorer, right? Check out the new online statement Want some quick tips on how you can boost your retirement planning with CPF? You can now find out what you can do by logging in to the myCPF portal with your SingPass to read your newly improved digital CPF yearly statement of account. Instead of just showing your balances in the Special, Ordinary, MediSave and Retirement (for those 55 years and above) accounts, the statement also comes with pointers on how you can improve your financial planning. With these reminders, you can: Learn how you can build up your own or your loved ones retirement savings by transferring your CPF savings from your Ordinary Account to your Special or Retirement accounts, or use cash top-ups to enjoy tax relief. Have an overview of the contributions you received into your CPF accounts in 2020. This is especially important for those who are self-employed so that they dont miss out in setting aside such savings. Check how much of the fund you have used for other purposes, such as home loans or medical expenses. If you realise too much money has been withdrawn for your home loan, you may want to use more cash instead so that your balances in CPF can increase. Plan for your retirement, if you are 55 and above. Your balance in your Retirement Account will give you an idea of the size of your CPF Life monthly payout after 65. Find out how much government support you had received in cash payouts from schemes administered by the CPF Board. Those who want more tips in CPF planning can also log on to this website.

|

|

#182

03-01-2021, 11:30 PM

|

|||

|

|||

|

Re: How much money needed to Retire?

Quote:

I notice at different stage of your life, you see this differently. When I was young I blame the government and adore the western world As I grow up and work there, I totally reverse this view. At any time, I will choose to be in Singapore even though I got my Australia PR and stayed there for about 4 years. Total waste of time, money and effort. It is a place that I do not want my kids to grow up in.

|

|

#183

03-01-2021, 11:32 PM

|

|||

|

|||

|

Re: How much money needed to Retire?

Quote:

Which we did what most kids will do, we return it all to my mother. You pass on, does not mean the CPF goes to government. So don't panic.

|

|

#184

03-01-2021, 11:35 PM

|

|||

|

|||

|

Re: How much money needed to Retire?

Quote:

I urge you to compare again. My dad was the first generation migrated from HK. Until today, I still have part of my relatives in HK. Their housing and living condition there...... it is a lot more challenging than ours.

|

|

#185

03-01-2021, 11:45 PM

|

|||

|

|||

|

Re: How much money needed to Retire?

Don't get me wrong. I am not saying our government is perfect. They have their flaws too.

But then again, no one is perfect. I can only choose a place that I can best make a living with and raise a family. My priority was education and safety. For these two things, our country fit it perfectly.

|

|

#186

04-01-2021, 01:43 AM

|

|||

|

|||

|

Re: How much money needed to Retire?

Quote:

|

|

#188

04-01-2021, 11:35 PM

|

|||

|

|||

|

Re: How much money needed to Retire?

i don't understand your examples, isn't RA = BRS/FRS/ERS?

RA is the account where you deposit the amount that you choose (BRS/FRS/ERS) interest in RA is 4% Quote:

|

|

#189

05-01-2021, 03:50 AM

|

||||

|

||||

|

Re: How much money needed to Retire?

Thanks Bro for sharing CPF hack. I like the idea of investing out the SA first to prevent deduction from RA den putting it back to SA, enjoying 4% and the flexibility of withdrawing one shot any time you need. Not a real fan of RA though in maxing to ERS since you will almost certainly not able to spend it all before you die. RA at BRS will do in my opinion.

Quote:

|

|

#190

07-01-2021, 12:27 PM

|

|||

|

|||

|

Not sure if this has been posted, but ideally, the amount varies for all people, more importantly depending on the person's lifestyle and expenditure.

My take on a formula should be something more like 100 years old - ( Retirement Age ) = A Amount of expenditure per month, excluding all the stuff that assumingly will be paid off when you are retired, inclusive of your leisure, entertainment expenses, insurance etc = B x 12 Conservatively, the amount should be A x (B x 12) = This amount should be a rough estimate.

|

|

#191

07-01-2021, 02:03 PM

|

|||

|

|||

|

Re: How much money needed to Retire?

After retirement, it is the life style you choose to live.

You also need to adjust spending habit and expectations. The basic need - food and household utilities - are taken care of, then surplus is how you want to spend it. As long as you don't live hand to mouth then retirement is peaceful. Quote:

|

|

#192

07-01-2021, 02:41 PM

|

|||

|

|||

|

Re: How much money needed to Retire?

how much money is hard to say, it solely depends on the quality of life that you wish to live on

|

|

#193

08-01-2021, 08:05 PM

|

|||

|

|||

|

Not many cpf members would saved the $, and not withdraw it for spending. Is this the reasons of increase buyers for EC? COE also saw an increase, probably members taking out $ to buy cars.

This is the year with the biggest group of people who turned 55.

|

|

#194

08-01-2021, 11:23 PM

|

|||

|

|||

|

Re: How much money needed to Retire?

Quote:

BRS = Basic Retirement Sum FRS = Full Retirement Sum (2x BRS) ERS = Enhanced Retirement Sum (1.5x FRS, 3x BRS), also called the top-up limit to your RA for that year.. ERS will increase every year to allow ppl to top up more if they want to. CPF don't force you to top up, you can choose not to if you don't want. All these are the sums that you tried to hit in order to receive a comfortable monthly payout when you reach your payout eligibility age. Also, the govt has being given extra 1% interest to RA when you are above Age 55, below Age 55 is to SA. And another 1% for the elderly (RA). So actually is more towards up to 6% interest. The thing I presume the other bro was saying is the CPF LIFE annuity, which for most of us will only need to choose closer to Age 65. So now just slowly save up your nest of retirement funds can liao.. Plus CPF has a consultation service for retirement planning, why don't you guys go and use the free service? lol..

Last edited by JizFries; 08-01-2021 at 11:25 PM. Reason: add on the portion on RA interest

|

|

#195

08-01-2021, 11:26 PM

|

|||

|

|||

|

Re: How much money needed to Retire?

Quote:

https://www.channelnewsasia.com/news...ement-13327948

|

| Advert Space Available |

|

|

| Bookmarks |

|

|

t Similar Threads

t Similar Threads

|

||||

| Thread | Thread Starter | Forum | Replies | Last Post |

| Can use CPF money to retire this way? | Sammyboy RSS Feed | Coffee Shop Talk of a non sexual Nature | 0 | 05-09-2019 12:50 AM |

| Expensive F-35s. Money is needed for other things. | Sammyboy RSS Feed | Coffee Shop Talk of a non sexual Nature | 0 | 21-09-2015 03:00 PM |

| Expensive F-35s. Money is needed for other things. | Sammyboy RSS Feed | Coffee Shop Talk of a non sexual Nature | 0 | 21-09-2015 02:30 PM |

| Expensive F-35s. Money is needed for other things. | Sammyboy RSS Feed | Coffee Shop Talk of a non sexual Nature | 0 | 21-09-2015 02:10 PM |

| help a Philippines girl, She needed money. | artist | The Malaysian Commercial Sex Scene | 36 | 06-02-2011 11:56 PM |